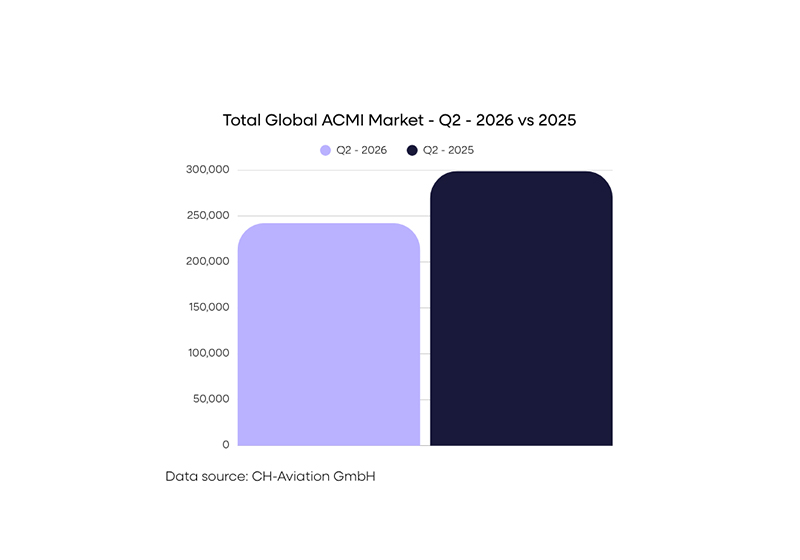

The global ACMI (Aircraft, Crew, Maintenance and Insurance) market experienced a notable slowdown during Q2 2026, with total block hours declining by 18.9% year-on-year compared with the same period in 2025.

While the downturn reflects broader market pressures across the aviation industry, ACC Aviation’s latest market analysis highlights significant regional and fleet segment variations that reveal an evolving ACMI landscape rather than a uniform contraction.

According to ACC Aviation, geopolitical instability across the Middle East, combined with changing airline operating strategies, softer booking trends, and increased cost pressures, contributed to reduced ACMI demand across several core markets.

“The market slowdown in Q2 was broadly anticipated given the external pressures affecting airline operations globally. ACMI demand has always responded quickly to shifts in airline confidence, network planning, and operational requirements, and this quarter demonstrated that dynamic clearly,” commented Dave Williams, Director of Leasing at ACC Aviation.

Europe Drives Overall Market Decline While South America Shows Growth

Europe remained the largest ACMI customer region in Q2 2026, accounting for 50% of global demand, however total European block hours declined by 25.8% year-on-year, reducing its overall market share from 54% in Q2 2025.

Asia demonstrated greater resilience, declining by 7.3% year-on-year while increasing overall market share to 23%. North America experienced the sharpest regional contraction with demand falling 60%, while South America delivered the strongest relative growth at 51% year-on-year, albeit from a smaller market base.

“Europe continues to be the core of the ACMI market, so changes in European demand disproportionately influence global performance. What we are seeing now is airlines becoming more selective and strategic in their ACMI deployment rather than pursuing broad seasonal coverage,” Williams added.

Narrowbody Weakness Offsets Continued Widebody Momentum

Fleet data shows narrowbody aircraft remained the principal driver behind the market decline, with utilisation reducing by almost 34% year-on-year.

The most established ACMI platforms saw significant reductions including:

• A320 CEO: –46%

• B737-800: –28%

• A321: –58%

• B737 MAX 8: –81%

By contrast, the widebody ACMI segment delivered 20.2% year-on-year growth, supported by more structured contract planning.

Growth highlights included:

• A330-300: +17%

• B777-200ER: +35%

• B787-9: +452% (from a smaller market base)

• A330-900neo: +83% (also a smaller market base)

• A330-200 was -2.6% and B777-300ER was -34%

“The standout trend from Q2 is the continued resilience of widebody ACMI. Unlike some narrowbody deployment, widebody contracts are increasingly being secured as part of longer-term operational planning rather than purely reactive capacity solutions,” Williams said.